The Federal Reserve cuts interest rates again but remains divided over future policy, creating uncertainty for consumers watching mortgage rates today. Here’s how the latest decision could affect loans, housing, inflation, and markets.

INTRODUCTION: A NEW TURNING POINT AS THE FED CUTS RATES AGAIN

The Federal Reserve has cut rates again, marking another significant step in its ongoing attempt to balance economic growth, inflation pressures, and financial market stability. As policymakers delivered the latest reduction, one question dominated public attention: What does this mean for mortgage rates today? Many households, investors, and analysts immediately turned their focus toward how the new decision would influence borrowing conditions, home financing options, and broader consumer sentiment. With the Fed now openly divided over future rate moves, the debate surrounding inflation control, economic cooling, and lending conditions is intensifying.

In today’s financial environment, mortgage rates today have become one of the most closely monitored indicators of economic health. Each Fed meeting sends ripples through loan markets, affecting homebuyers, refinancing trends, construction demand, housing inventory, and affordability. As this latest rate cut reverberates across the economy, conversations about mortgage rates today have grown even more urgent. Consumers want to know whether rates will drop further, stabilize, or reverse — especially as policymakers disagree on what comes next.

With inflation cooling but still above target, the labor market adjusting, and global economic pressures mounting, the Fed’s split opinions make evaluating mortgage rates today more complex than ever. This article breaks down everything that matters: the Fed’s reasoning, internal disagreements, economic forecasts, housing implications, and the long-term outlook for borrowers navigating the volatile landscape of mortgage rates today.

SECTION 1: WHAT THE FED ANNOUNCED — AND WHY IT MATTERS FOR MORTGAGE RATES TODAY

The Federal Open Market Committee (FOMC) delivered the latest rate cut by a narrow margin, reducing the benchmark federal funds rate for the second consecutive meeting. This decision signals that the central bank is leaning toward supporting economic growth as inflation moderates, yet the split vote reveals uncertainty beneath the surface.

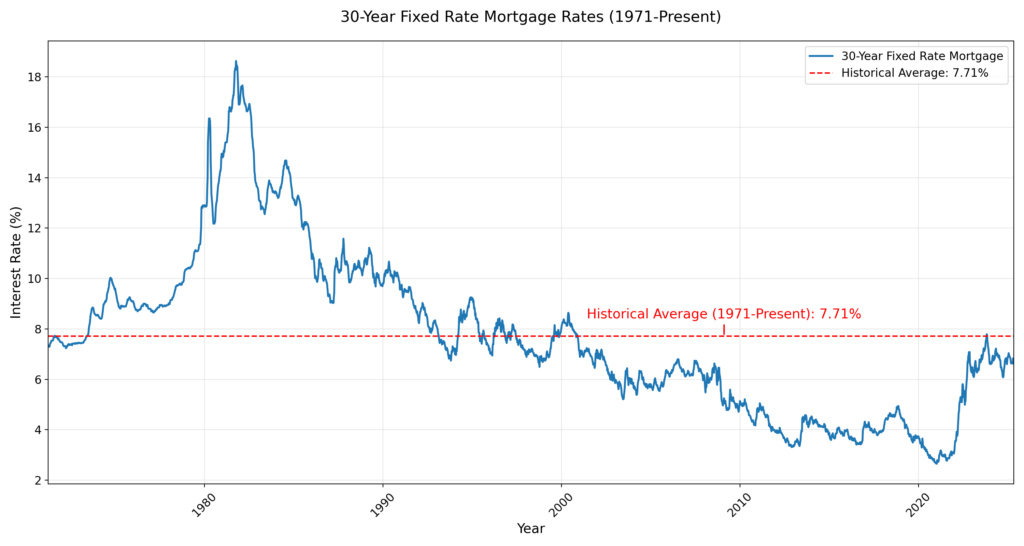

One of the biggest concerns tied to the announcement is how the cut will influence mortgage rates today. Historically, mortgage rates do not move in perfect lockstep with Fed decisions, but they do respond to broader trends in the bond market — especially 10-year Treasury yields, which are heavily influenced by Fed communication, inflation expectations, and recession risks.

In recent weeks, mortgage rates today have fluctuated between relief and hesitation. Some lenders priced in anticipation of a rate cut, while others remained cautious due to contradictory economic signals. With the Fed confirming the cut, mortgage rates today may see short-term relief, but analysts warn that further movement will depend on incoming economic data and the degree of disagreement within the Fed’s ranks.

This divergence among policymakers — some urging more cuts, others arguing to pause — adds volatility. Homebuyers and refinancers tracking mortgage rates today will face heightened uncertainty until the central bank articulates a clearer long-term stance.

SECTION 2: WHY THE FED IS DIVIDED — COMPETING ECONOMIC PRIORITIES

Not all policymakers agreed with the rate reduction. Several officials expressed concern that inflation, though easing, remains too elevated to justify a series of cuts. Others stressed that the economy is showing signs of slowing and that failing to cut could risk a sharper downturn.

This tension creates ripple effects across financial markets and directly influences expectations around mortgage rates today. Some members believe that cooling inflation supports further easing, which could help lower mortgage rates today and stimulate housing demand. Conversely, more cautious policymakers argue that aggressive cuts could reignite inflation and force future rate hikes, potentially pushing mortgage rates today higher again.

These differing philosophies stem from several conflicting data patterns:

1. Inflation Cooling but Not Yet at Target

While the overall trend is downward, core inflation remains sticky in key sectors. This complicates predictions for mortgage rates today, as bond markets react strongly to inflation trajectory.

2. Labor Market Showing Early Cracks

Employment data suggests slowing job growth, which typically supports lower rates — potentially bringing relief to mortgage rates today.

3. Manufacturing Weakness vs. Consumer Strength

Parts of the economy remain soft while others are resilient, making forecasting rates challenging.

4. Global Pressures

Geopolitical tensions and international slowdown add unpredictability, influencing foreign demand for U.S. bonds — and by extension, mortgage rates today.

Because of these forces, Fed officials remain split, and the future path of mortgage rates today hinges on which side ultimately gains more influence in the upcoming meetings.

SECTION 3: HOW FINANCIAL MARKETS REACTED — AND WHAT’S NEXT FOR MORTGAGE RATES TODAY

Markets responded instantly to the rate cut. Treasury yields dipped, equities surged briefly, and mortgage-backed securities experienced moderate volatility. As these markets recalibrate to the Fed’s messaging, the direction of mortgage rates today is beginning to take shape.

Mortgage lenders quickly adjusted pricing models, with several hinting at small decreases over the coming days. While this movement is positive for borrowers monitoring mortgage rates today, it is not yet a dramatic shift. Experts caution that until the Fed unifies its stance or inflation drops more sharply, mortgage rates today will likely continue experiencing week-to-week fluctuations.

Financial analysts also note that long-term mortgage products remain sensitive to economic sentiment. Any sign of recession fears or inflation rebounds could push mortgage rates today higher again. Conversely, more evidence of cooling inflation would likely pull them lower.

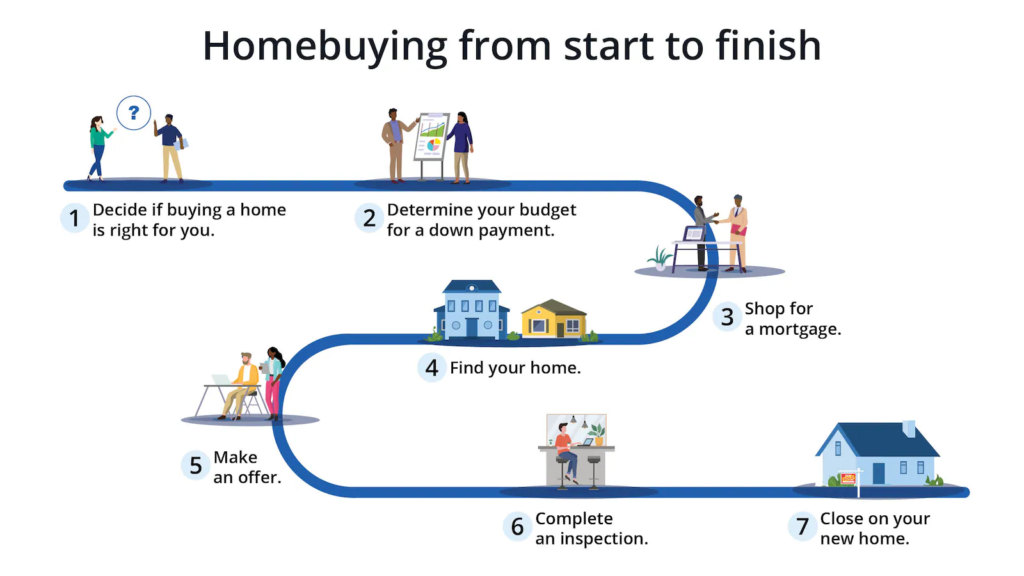

SECTION 4: HOUSING MARKET IMPACT — BUYERS, SELLERS, AND BUILDERS RESPOND

The U.S. housing market is in a unique moment as mortgage rates today react to the Fed’s ongoing policy shifts. With affordability at decade lows and home prices still elevated, even a small drop in mortgage rates today can change buyer behavior dramatically.

Homebuyers Feel Renewed Hope

For months, many potential buyers have been locked out due to high borrowing costs. The possibility of more rate relief has made mortgage rates today a trending topic among first-time buyers and investors alike. Lower rates mean lower monthly payments — often the difference between qualifying and not qualifying for a loan.

Home Sellers Reevaluate Pricing

As mortgage rates today ease, sellers may see increased foot traffic and stronger offers, particularly in mid-priced markets where affordability is tightest.

Builders Adjust New Project Plans

Construction companies closely watch mortgage rates today to determine demand strength. Rate cuts historically stimulate new builds, easing inventory shortages.

Investors Enter or Exit the Market

Real estate investors assess cap rates against mortgage rates today. Lower rates can improve ROI calculations, triggering more purchases in rental-heavy markets.

Because the housing sector is highly interest-rate-sensitive, every small shift in mortgage rates today can reshape supply, demand, and pricing patterns across the nation.

SECTION 5: WHAT CONSUMERS SHOULD DO NOW — STRATEGY FOR NAVIGATING MORTGAGE RATES TODAY

With uncertainty ahead, experts recommend:

✔ 1. Lock a Rate if You’re Comfortable

Given slight downward movement in mortgage rates today, locking a favorable rate could protect borrowers from sudden reversals.

✔ 2. Monitor Economic Data Releases

Inflation, employment, and GDP reports heavily influence mortgage rates today.

✔ 3. Shop Multiple Lenders

Rate variations widen during volatile periods — comparing lenders can save thousands.

✔ 4. Consider Adjustable-Rate Mortgages (ARMs)

If mortgage rates today trend downward gradually, ARMs may provide short-term savings.

✔ 5. Evaluate Refinancing Opportunities

Homeowners paying older, higher rates should track mortgage rates today weekly to capture future dips.

With the Fed uncertain about its path, consumers must stay vigilant and informed.

Frequently Asked Question (FAQs):

Q1: Why did the Fed cut rates again?

To support slowing economic conditions while inflation cools. The move creates opportunities for lower borrowing costs, including mortgage rates today.

Q2: Are mortgage rates today guaranteed to drop?

Not guaranteed — but they may trend slightly lower depending on inflation data, bond yields, and Fed guidance.

Q3: Why is the Fed divided?

Policymakers disagree on inflation risk vs. economic slowdown risk, leading to uncertainty affecting mortgage rates today.

Q4: Will housing become more affordable soon?

Affordability may improve if mortgage rates today decrease, but home prices remain high in many markets.

Q5: Should I refinance now?

It depends on your current rate and financial goals — track mortgage rates today and consult lenders.